Investing safely in 2025–2026 means more than picking the right broker — it also means understanding the role of regulators. The Financial Conduct Authority (FCA) is the main body overseeing financial services in the UK. Its purpose is to ensure markets operate fairly, protect consumers, and maintain trust in the financial system.

But how reliable is FCA in practice, and can it help investors recover lost funds? Let’s break it down.

What is FCA and How It Works

The FCA regulates thousands of firms offering financial products in the UK, from banks and brokers to fintech startups. Unlike regulators in other regions, FCA combines consumer protection with strict market supervision. Its key tasks include:

- licensing companies to operate legally in the UK;

- monitoring firms for compliance with financial rules;

- protecting investors from misleading or fraudulent activity;

- publishing warnings and guidance for consumers.

In short, FCA sets the rules, oversees compliance, and steps in when companies fail to meet standards — but it does not act as a personal recovery service.

How to Obtain an FCA License

For companies, obtaining an FCA license involves multiple steps. A firm must:

- Submit detailed business plans and compliance documentation.

- Demonstrate sufficient capital reserves and operational capability.

- Pass thorough background checks for all directors and key staff.

- Agree to ongoing reporting and regulatory audits.

It’s important to note: private individuals cannot obtain an FCA license. Licenses are strictly for companies offering regulated financial services. Anyone claiming otherwise is likely misinforming potential investors.

Official FCA Website Overview

The FCA’s official portal, fca.org.uk, is a central hub for information. Key features include:

- A Firm Register to verify licensed companies.

- Alerts and warnings about unauthorised firms.

- Guides for consumers on investing safely.

- Contact channels for complaints and reporting misconduct.

Knowing how to navigate the site is crucial for verifying brokers and avoiding scams.

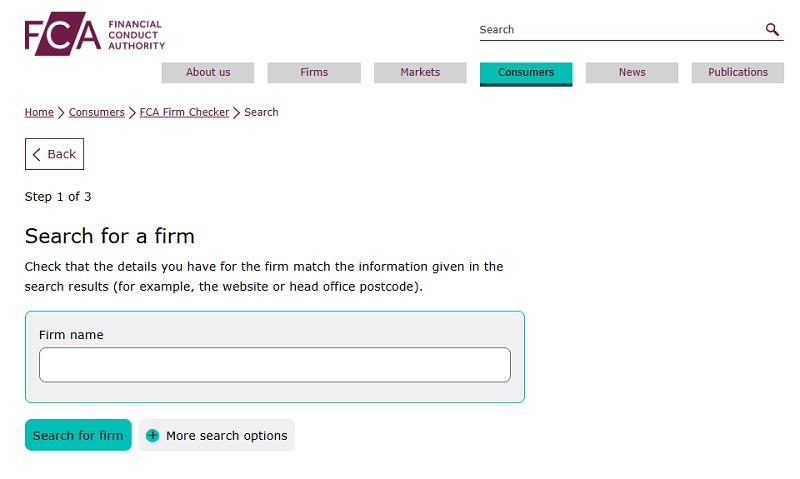

How to Verify a Broker’s FCA License

Before trusting a broker, investors should take these steps:

- search for the company in the FCA Firm Register using its legal name;

- confirm registration numbers and license type;

- check for any active warnings or past enforcement actions;

- compare the license information with documents provided by the broker.

Red flags of fake licenses include mismatched registration numbers, unofficial-looking documents, or pressure to bypass official verification.

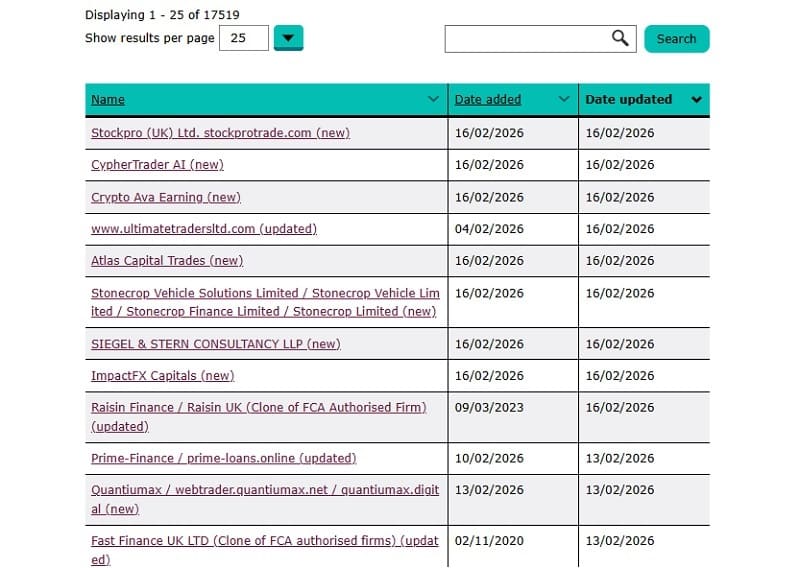

FCA Blacklist and Warning Notices

Contrary to some assumptions, the FCA does not maintain a single “blacklist” of firms or individuals that have violated rules, similar to consolidated registers that exist in some other countries. There isn’t a public list where every breach or infraction is catalogued. However, the FCA provides several specialized tools and lists that investors can use to assess risk and avoid problematic companies.

Key FCA Tools for Checking Firms

- Warning List

This list highlights firms whose operations have raised concerns among regulators.

Inclusion doesn’t automatically mean the company is fraudulent, but it signals potential risk.

The list is updated frequently, allowing investors to stay aware of changing circumstances and avoid companies that may be experiencing regulatory difficulties.

- Unauthorised Firms List

This is a compilation of companies operating without proper FCA authorization.

Even if some of these companies provide quality services, engaging with them is inherently risky because they lack regulatory oversight.

For safety, it’s recommended to prefer firms that are officially registered and compliant with FCA rules and legislation.

- ScamSmart

ScamSmart is a dedicated page that educates consumers about known and emerging scams in the financial sector.

It covers tactics scammers use to lure naive or inattentive investors.

Since fraudulent methods evolve rapidly, regularly consulting ScamSmart helps users stay informed and avoid falling victim to new schemes.

How to Use FCA Lists Effectively

All FCA lists are regularly updated, and the information is verified by the regulator, making them reliable tools for pre-investment checks. The FCA website’s search function allows you to find mentions of companies in any context. This is a straightforward tool, but remember to:

- search in English, and

- check for alternate names or variations of the company name to ensure nothing is missed.

By combining these tools, investors can make better-informed decisions and significantly reduce the likelihood of engaging with a risky or unauthorized financial service provider.

Can FCA Help You Recover Money From a Broker?

It’s important to understand that the FCA does not hold your funds and cannot directly compensate you if you simply transferred money to a broker. Its role is regulatory, meaning it oversees companies to ensure they follow financial laws and protect consumers — but it does not act as a personal bank or recovery service.

When FCA Can Assist

While the FCA does not return money directly, there is a mechanism for compensation through the Financial Services Compensation Scheme (FSCS). This scheme protects clients of certain financial companies if the company is FCA-licensed, fails, or becomes insolvent.

Key points about FSCS:

- Compensation can cover up to £85,000 per person, per company.

- The company must be officially registered and authorized by the FCA.

- Only licensed UK-based firms are covered.

If the broker is unregistered, operates offshore, or is a fake/bogus broker, neither the FCA nor FSCS can return your funds.

What to Do if You’ve Sent Money to a Scam Broker

If your funds have been sent to an unlicensed or fraudulent broker, FCA’s role is mainly preventive and advisory, not restorative. For example, FCA can:

- Issue public warnings about the company and add it to the “alert list”.

- Support investigations in cooperation with law enforcement authorities.

- Advise on formal complaint procedures against licensed firms.

However, FCA cannot guarantee that you will get your money back.

How Recovery Usually Happens

In reality, recovering money from scammers often requires alternative approaches:

- Bank or card chargebacks — if payment was made via credit or debit card, sometimes banks can reverse the transaction.

- Specialized recovery companies — such as crypto recovery or fraud recovery services, which attempt to trace and recover lost funds.

- Legal action — filing lawsuits against registered intermediaries if they were involved in the transaction.

FCA Communication: What They Will and Will Not Do

Another common confusion revolves around how FCA communicates:

- Official channels only: FCA communicates through its website, official email addresses, and formal correspondence. Investors should expect no private messages from staff on social media, Telegram, WhatsApp, or phone calls unless the interaction is initiated through verified FCA contact forms.

- What FCA will do: They provide guidance, respond to formal complaints, issue warnings, and publish regulatory updates.

- What FCA will not do: FCA staff will never ask for private login details, passwords, or crypto wallet access, nor will they promise fund recovery. Any message claiming to be from FCA requesting these is a scam.

Always verify the contact. Check email domains, use official forms, and cross-reference any claim with the FCA website before responding.

Clear understanding of communication boundaries helps investors avoid falling for FCA impersonation scams, which are increasingly common, especially targeting people who have already suffered financial loss.

Conclusion

Understanding FCA’s real capabilities helps investors separate fact from fiction and make informed, safer choices. Verification, caution, and reliance on official sources remain the best protection in 2025–2026 financial markets.